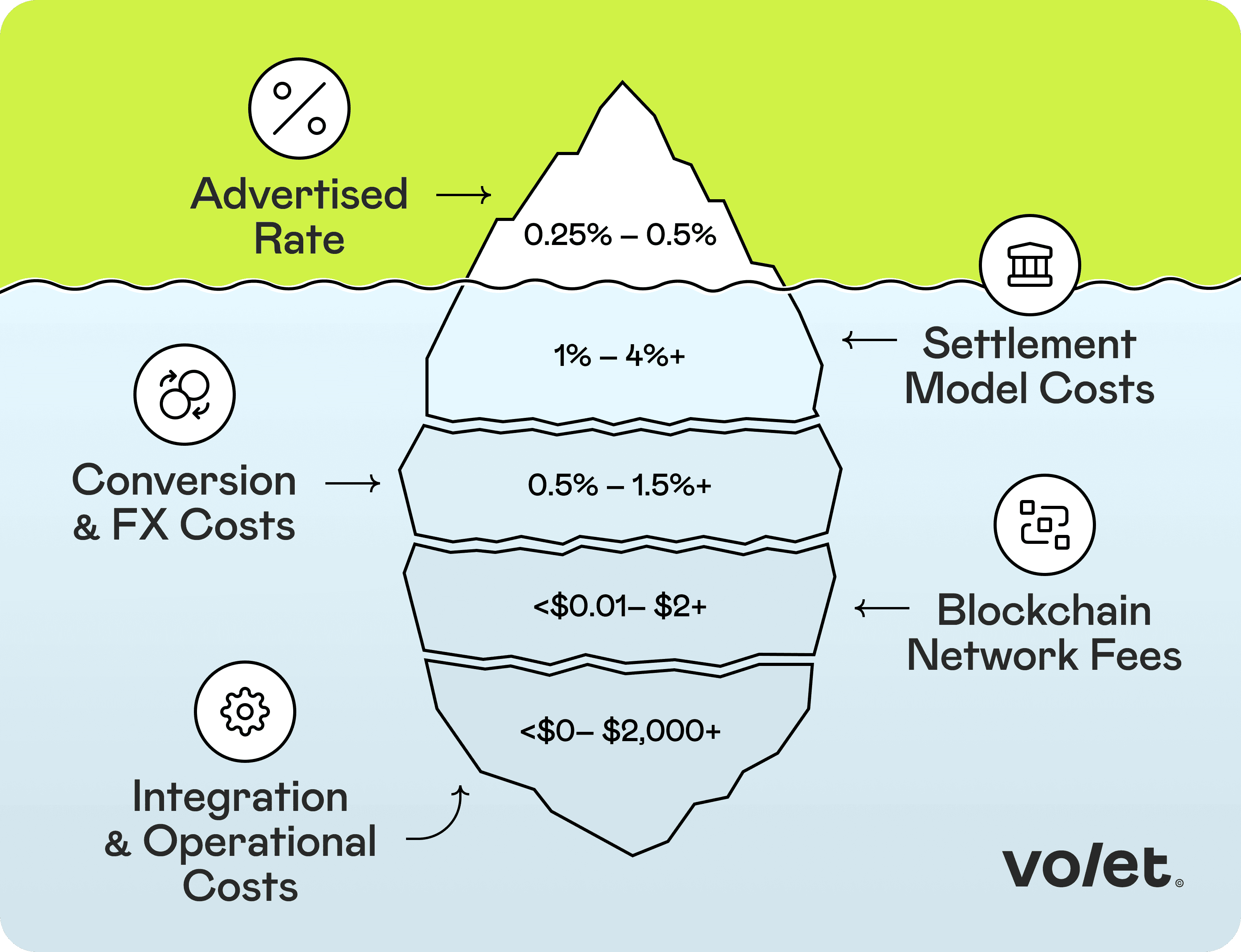

Most merchants who switch to crypto acquiring expect to save money. Many do, but often not as much as the advertised rate suggests. Because that rate is only the tip of the iceberg.

Crypto payment processing promises lower fees and no chargebacks. For many online businesses, those promises hold up. But only if you understand the full cost picture before you commit. The headline rate your gateway advertises is rarely the only number that matters. In fact, there are several other categories of costs that affect what you actually pay. Here's a complete breakdown with real numbers, so you can compare your options accurately.

Key Takeaways

Before committing to a crypto payment gateway, get answers to these specific questions:

1️⃣ What is the all-in rate for settlement to my bank account in EUR/USD? (Not the rate for on-chain settlement to a crypto wallet.)

2️⃣ What is your FX spread on crypto-to-fiat conversion? (Ask for a worked example with a real amount.)

3️⃣ When are funds actually available in my bank account? (Not when is the payment confirmed on-chain. Those are two different events.)

4️⃣ Are there setup fees, monthly platform fees, or minimum volume commitments?

5️⃣ Does your hosted checkout solution cover compliance on your side?

6️⃣ What does integration look like? API only, or are there CMS plugins and hosted checkout options?

The real cost of accepting crypto payments can be several times higher than the advertised rate

🎭 Settlement Costs: The Fee Behind the Fee

This is the biggest source of confusion in crypto payment processing, and the one most gateway providers obscure.

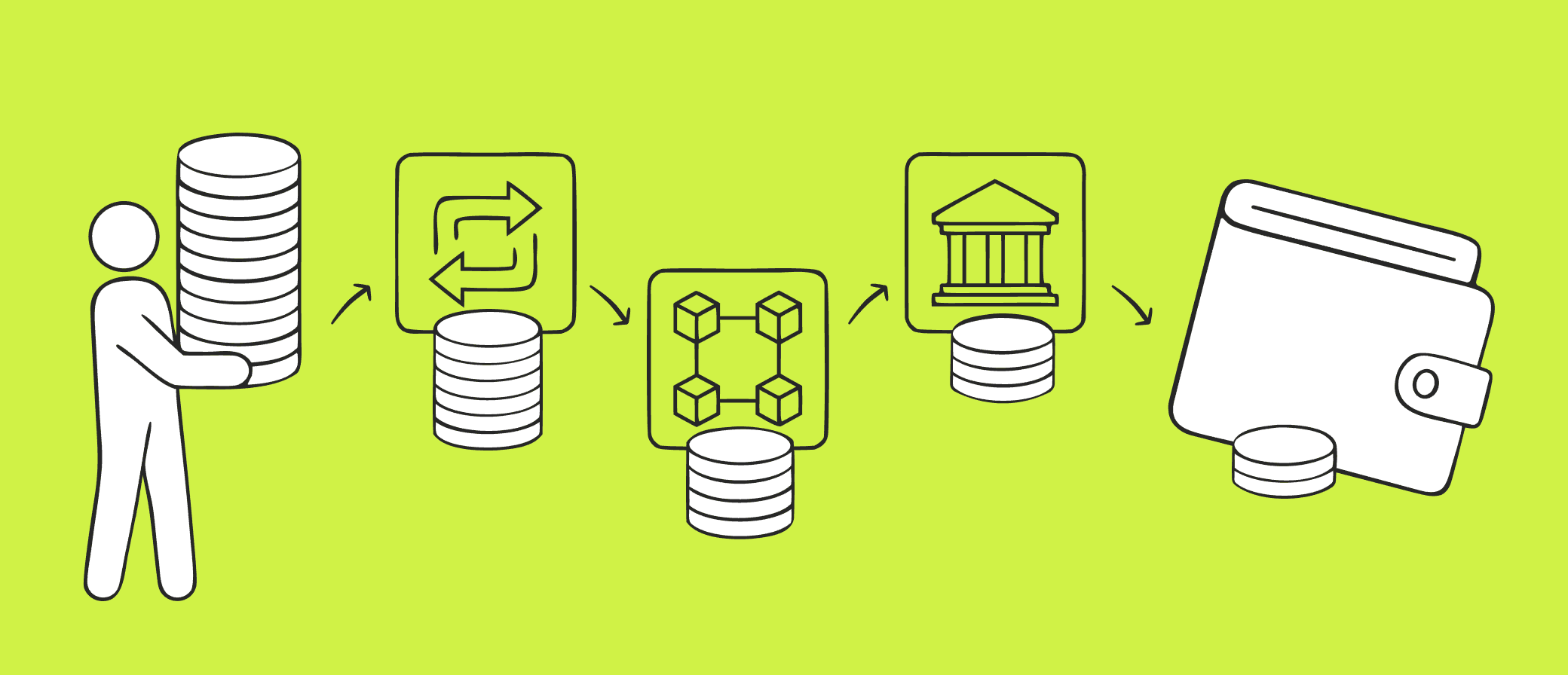

When a customer pays in USDT or BTC, the funds don't automatically appear in your bank account. They have to go somewhere first. Every step in that journey carries a cost. There are three common models:

Non-custodial settlement means crypto goes directly to your own external wallet via smart contract, no intermediary involved. Payment processing fees are typically 0.5%, though high-volume merchants can negotiate rates from 0.25%. At Volet.com, the rate is a flat 0.25% regardless of volume.

One important detail: with non-custodial settlement, you receive crypto — not fiat. Converting that to fiat and sending it to your bank account is a separate step that typically costs another 2–4% in crypto conversion fees and spreads.

There's also a crypto volatility risk if you accept anything beyond stablecoins. Say a customer pays $100 for your service in BTC. At the moment of payment, you receive roughly 0.0013 BTC. A few weeks later, when you go to convert it, the price has dropped. So that 0.0013 BTC is now worth $75. Non-custodial settlement puts that currency risk entirely on you.

Custodial settlement to a crypto wallet means funds are held by the provider in an internal wallet in your account. The upside: custodial wallets typically offer faster and more cost-effective tools for converting crypto to fiat and withdrawing to a bank account.

Payment processing fees for custodial settlement are usually 0.25–0.5%. At Volet.com they are 0.25% flat.

Some providers also offer auto-conversion of incoming crypto into stablecoins to reduce your price exposure. At Volet.com, auto-conversion into USDT or USDC costs 1%.

From the custodial wallet, withdrawing to an external crypto wallet typically costs only the network fee. But withdrawing to a bank account usually involves a conversion fee (0.5–1%) plus a withdrawal fee (1–1.5%).

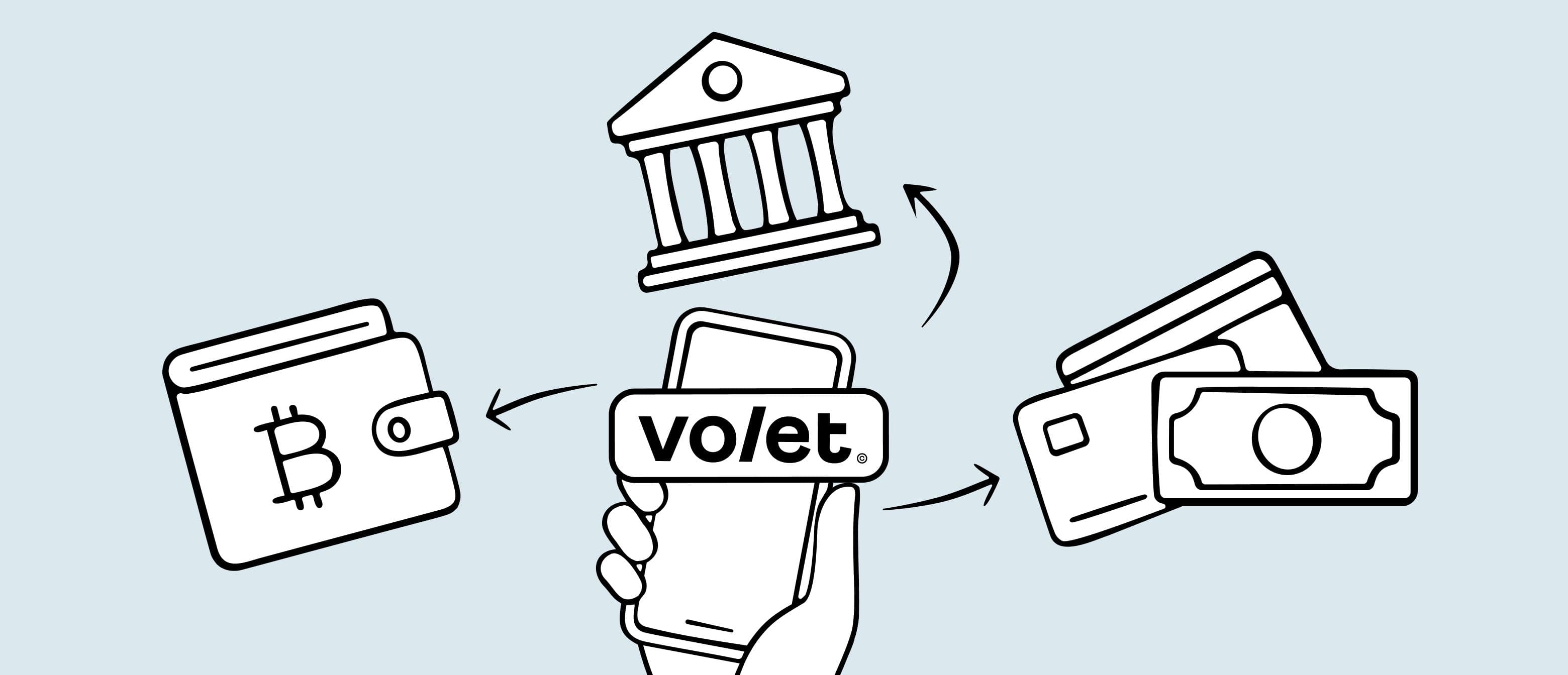

With Volet.com you can accept crypto with automatic conversion directly into USD or EUR, credited to your Volet.com account. This simplifies the cost structure considerably. For USD withdrawals, the typical all-in cost is 1.25–1.75%:

▪️ Crypto acquiring: 0.25%

▪️ Conversion to USD: 0% for stablecoins, 1% for other crypto

▪️ Withdrawal to bank account: 1–1.5% depending on country and rails

One more advantage of this model: fiat is withdrawn via standard payment rails from a legal entity. The payment your bank receives comes through an official payment system — not from a crypto address. Your banking counterparties have no visibility into the crypto layer at any point.

Custodial settlement to a bank account means incoming crypto is automatically converted to fiat and sent directly to your bank. The cost structure here has three components:

▪️ Crypto acquiring: 0.25–0.5%

▪️ Auto-conversion to fiat: ~1.5%

▪️ Bank transfer fee: 1–1.5%

This is where the advertised rate creates the most confusion. A provider may offer custodial-to-bank settlement with full auto-conversion, but advertise only the non-custodial acquiring rate (the lowest number in their pricing). The real difference between these two models can be 3 percentage points. On a $250,000/month volume, that's $7,500 per month in costs you didn't model.

💱 Conversion and FX Costs: The Invisible Spread

If your business operates in fiat currency, at some point your crypto receipts have to be converted. This conversion carries a cost, but it's rarely listed as a line item.

Providers typically quote something like "near-market rates" or "low FX spread." What this means in practice varies significantly. A spread of 0.5% on a $100,000 conversion is $500. A spread of 1.5% is $1,500. On a platform processing $1M/month, the difference between providers on this single variable can exceed $10,000/month.

Another thing to consider iscrypto volatility. If there's a delay between a customer paying in BTC and you converting to USD, the exchange rate can move against you. A customer pays $500 worth of BTC at 3pm. By the time your provider processes and converts it at the end of the day, BTC has dropped 4% and you receive only $480. On a high-volume day with dozens of such transactions, the shortfall adds up before you've even looked at your payment gateway fee.

Stablecoins (USDT, USDC) reduce this risk: their value is pegged 1:1 to the dollar, so there's no exposure between receipt and conversion. For most online businesses, routing customers to stablecoin payment options is the simplest way to remove crypto volatility from the cost equation.

When comparing payment processing fees across providers, ask for the all-in cost for a specific transaction: currency in, currency out, amount. The provider willing to give you that number clearly is usually the one with less to hide.

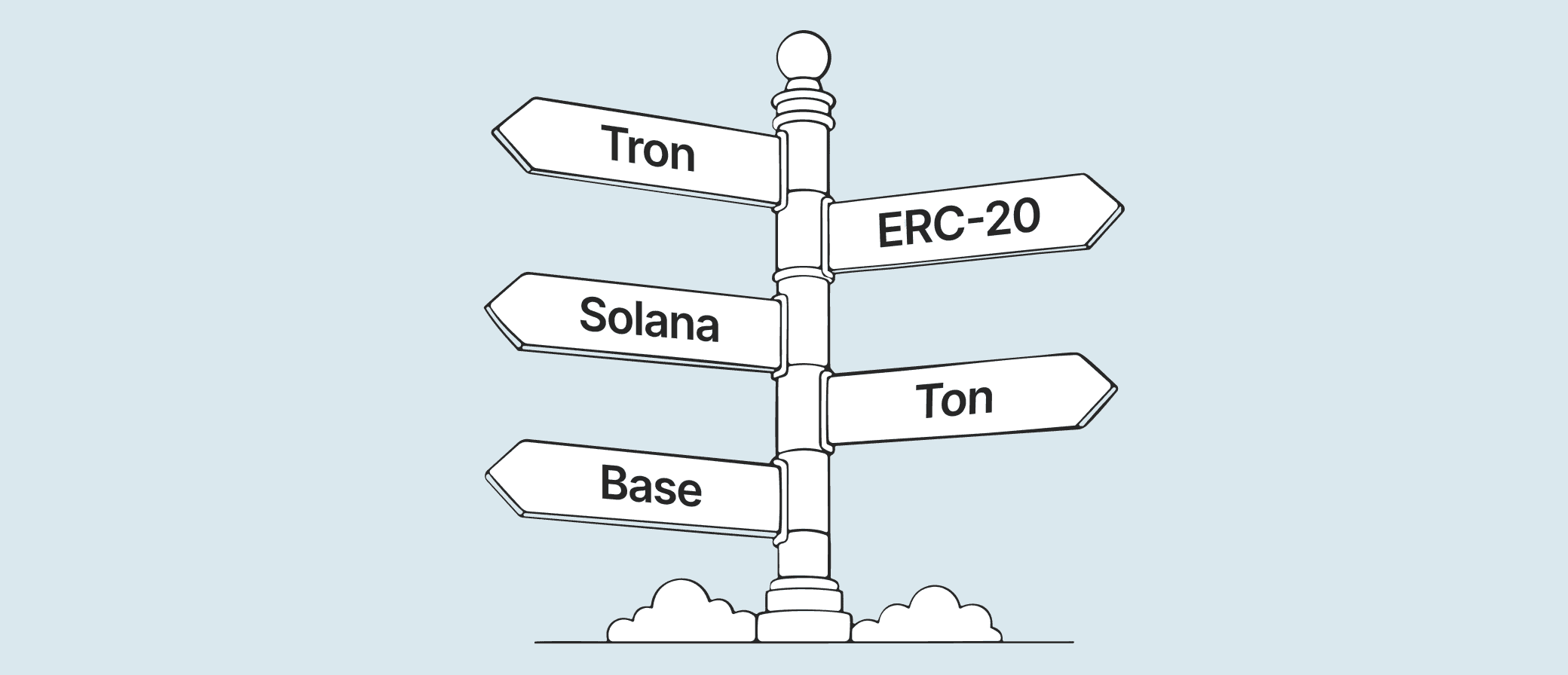

⛓️ Blockchain Fees: What the Network Charges

Blockchain fees (often called gas fees or network fees) are paid to validators on the network that processes each transaction. They are not set by your payment gateway. They are set by market conditions on the blockchain itself. But which blockchain your provider uses has a dramatic effect on what those gas fees cost.

Network

Typical fee per transaction

Arbitrum, Base (Ethereum L2)

$0.01–$0.30

Solana

< $0.01

TON

< $0.01

Ethereum L1

$0.05–$0.40 (can spike sharply under load)

Tron (TRC-20)

up to $2–$4

As a merchant, you will only have to pay blockchain fees in one case: if you receive cryptocurrency into a custodial wallet and want to withdraw it to a non-custodial wallet.

However, with every payment transaction, the blockchain fee will be paid by your customers. For small transactions, this fee can noticeably increase the total cost of your product in the eyes of customers.

For businesses receiving USDT

TRC-20 (Tron) is the most popular network by transaction volume, but also the most expensive for the sender. USDT is available on nine networks. TON and several Ethereum L2s all cost a fraction of a cent per transaction.

🛠️ Integration and Operational Costs: The Bill You Get Three Months Later

Payment gateway fees and transaction fees are the most visible costs. Integration and operational costs are the ones that surprise finance teams at the end of Q1.

Common categories:

Setup or monthly platform fees. Some processors charge $500–$2,000 to onboard a new merchant and then $50–$300 per month regardless of transaction volume.

This is uncommon in crypto payments. However, if you find an acquirer offering suspiciously low transaction fees, make sure there are no hidden fixed fees.

Developer time. A custom API integration at a blended developer rate of $100/hour is material even at 20 hours of initial work. Subsequent maintenance, webhook handling, and reconciliation tooling add more. No-code and low-code integration options (CMS plugins, hosted checkout pages) significantly reduce this line item.

Settlement speed. Providers often advertise "instant settlement" and on-chain confirmation is indeed fast. But there are two separate steps: crypto-to-fiat conversion (which with some providers, including Volet.com, happens near-instantly to the merchant's wallet) and fiat withdrawal to a bank account (which can take up to 3 business days via SWIFT or local rails). These are not the same event. When evaluating liquidity impact, ask specifically about when funds are available in your bank account, not just when the payment is confirmed.

Reconciliation overhead. Multi-currency, multi-network payouts create reconciliation complexity. How many formats does the provider export? Does it map to your accounting system? Manual reconciliation time has a real cost even if it doesn't appear on a gateway invoice.

Volet.com's Cost Structure

For reference, here is how Volet.com's pricing maps to the cost categories covered in this article.

Volet.com offers three ways to configure crypto acquiring:

1. Non-custodial settlement via smart contract. Crypto goes directly to your external wallet. The fee is a flat 0.25% regardless of payment volume. No additional charges. Converting that crypto to fiat is handled entirely on your side.

2. Custodial settlement to a crypto wallet in your Volet.com account. Receiving crypto into your Volet.com account costs 0.25%. If needed, you can enable auto-conversion of incoming crypto into stablecoins for an additional 1%. Withdrawing to fiat happens inside your Volet.com account and typically costs 1–1.5% depending on country and rails.

3. Custodial settlement to a fiat wallet in your Volet.com account. Incoming crypto is automatically converted not into stablecoins, but directly into USD or EUR. Crypto never touches your accounts at any stage. The fee structure for USD settlement: 0.25% for acquiring, 1% for conversion (only if you're accepting non-stablecoin payments), and 1–1.5% for withdrawal to a bank account. If you need conversion into EUR that's an additional 0.5% fee.

A few other things worth knowing about crypto acquiring with Volet.com:

▪️ No setup fees, no monthly platform fees, and no API access charges.

▪️ Full API for dev teams.

▪️ Hosted Checkout for low-code deployment, including in Telegram Mini Apps via webview.

▪️ Free CMS plugins for WordPress, WooCommerce, and OpenCart.

Scale your payments with Volet.com

Accept payments, send payouts, manage crypto and fiat across the globe — in one account.

Fee information is provided for general comparison purposes. Actual rates depend on volume, settlement method, and network conditions. Blockchain network fees are set by the respective networks and are not controlled by Volet.com. Always verify current pricing directly with any provider before making a decision.

FAQ

You don't need to replace anything. Crypto acquiring can run as an additional payment option alongside your existing card processor.

Most merchants start by adding a "Pay with crypto" option at checkout and keep card processing for customers who prefer it.

The two systems are independent: separate settlement flows, separate reconciliation. Integration time for adding crypto as a parallel option is typically a few hours for a simple setup, or one to two days for a larger service.

With providers that charge setup fees and monthly platform fees, there is a meaningful minimum. You need enough transaction volume to cover fixed costs before the per-transaction savings become real.

With providers that have no setup fees, no monthly fees, and no minimum volume commitments, the break-even point is much lower. At 0.25–1.75% acquiring versus 4–8% for high-risk card processing, even a few thousand dollars of monthly volume generates measurable savings.

For businesses just starting out, the more relevant question is integration cost: a no-code CMS plugin or a hosted checkout link can be live in under an hour, which makes the cost of testing essentially zero.

Crypto finality means the network cannot reverse a transaction, but your platform can still issue refunds. In practice, a refund is a new outgoing transaction from your balance to the customer's address, in the same or equivalent amount.

The practical considerations: who covers the exchange rate difference if the crypto price moved between payment and refund, and what address do you send the refund to.

Most platforms handle this by issuing refunds in stablecoins (USDT or USDC) to avoid crypto volatility exposure, and by collecting a refund address from the customer at the time of the dispute.

These are workflow decisions you configure on your side — the payment gateway processes the outgoing transfer the same way as any payout.

This depends heavily on how the settlement reaches your bank. If funds arrive as a wire from a crypto exchange or directly from a blockchain address, some banks will flag or delay the transfer pending AML review.

If funds arrive as a fiat transfer from a legal entity through standard acquiring rails (as is the case with Volet.com's settlement model) your bank sees an ordinary incoming payment from a corporate counterparty and has no visibility into the crypto layer.

That said, no provider can guarantee how any specific bank will treat incoming transfers, and it's worth notifying your bank relationship manager if you are making a significant change to your payment infrastructure.