Not scams, not FOMO — just mere operational mistakes.

Crypto scams get the headlines. Market crashes get the think-pieces. But beneath this surface lie the quiet, consistent money drain reasons most users never discuss. This article covers nine operational mistakes that cost freelancers, traders, and businesses real money in 2026 — and the rules that prevent each one.

The Pattern To Avoid

Every mistake on this list shares a common structure: a decision made by default rather than by intention.

The default network. The default withdrawal method. The default conversion timing. The default habit of copying from history. Each default was formed at some point for a reason — and then never revisited. The problem is not that defaults are wrong. The problem is that in crypto, the cost of an unconsidered default is paid immediately and in full — with no way back.

Traditional finance has correction mechanisms: overdraft reversals, dispute windows, customer service teams that can reach into a transaction and pull funds back. Crypto has none of these. A confirmed transaction is final.

The counter-habit is simple: before any transaction, run through four questions.

Pre-transaction checklist

Network — Did I confirm the recipient supports this network, not just the token?

Total cost — Did I add up processing fee + fixed fee + network fee + spread, not just the headline rate?

Method vs amount — Is this withdrawal method actually cost-effective at this specific amount?

Address — Did I verify all characters manually — not blindly copy from transaction history?

Thirty seconds on these four questions does save you a lot of money and hassle.

Mistake 1: Copying an Address From Transaction History

Transaction history feels like a safe source for wallet addresses. It is not.

Address poisoning works like this: an attacker sends a tiny dust transaction — often fractions of a cent worth of tokens — from a wallet address that closely resembles a recipient the user regularly pays. The lookalike address appears in the user's history, visually indistinguishable at a glance. The user copies it instead of the real one. In December 2025, one user lost $50 million USDT this way — among the largest single on-chain losses of the year.

Scammers' addresses may look almost identical to yours. Always check the full address

The amount involved does not change the mechanics. The same attack runs on a $500 transfer or a $50,000 one. The attacker's cost to poison an address is effectively zero — sending a dust transaction costs fractions of a cent on most networks — so the attack is not targeted at large wallets specifically. Anyone who copies addresses from transaction history is exposed, regardless of balance size.

The attack requires no technical access to the victim's wallet. It exploits one habit: copying addresses from history rather than from a saved contact or the original source.

💡 The rule: Verify all characters of any address manually before sending. Better: save trusted addresses to a whitelist in your wallet or platform, and send only from there. Never copy from transaction history.

Many wallets flag incoming dust transactions automatically — if you see an unsolicited micro-transfer from an unfamiliar address, treat it as a poisoning attempt and ignore it entirely. Do not interact with the address, do not send funds back, and do not copy anything from that transaction.

Mistake 2: Ignoring the Spread — Especially on Weekends

Most users know about fees. Fewer pay attention to the crypto conversion spread — the gap between the market rate and the rate a platform actually applies when converting crypto to fiat. Unlike a fee, it does not appear as a line item. It is simply the difference between what you received and what the mid-market rate would have given you.

Under normal weekday conditions, the spread on a USDT-to-USD conversion runs between 0.3% and 1.5%. On weekends, it gets meaningfully wider — and here is why.

Crypto markets run around the clock. Fiat settlement does not. When a platform converts your crypto to fiat on Saturday or Sunday, it cannot immediately settle with its banking partners. It is carrying exposure until Monday morning, and it prices that risk into the conversion rate. The same conversion that costs 0.5% spread on Tuesday may cost 2–3% on Saturday — not because the market moved, but because of how fiat settlement infrastructure works.

USDT-to-USD conversion rate over the week

The timing is an easy trap to fall into. Weekends are exactly when many freelancers and remote workers sit down to handle finances. If you received a payment on Friday and convert on Sunday, you are paying a spread premium simply because of when you logged in.

💡 The rule: When timing is flexible, convert on a weekday — Tuesday through Thursday is the lowest-cost window. Before any significant conversion, check the mid-market rate on CoinGecko and compare it to your platform's offered rate.

Mistake 3: Overlooking Inactivity Fees on Custodial Platforms

Many custodial platforms charge a monthly inactivity fee if the account sits dormant for six months or more. The fee is disclosed in the terms of service. It rarely appears in the onboarding flow.

On small balances — $50 to $150 — a $1 to $2 monthly inactivity fee erodes holdings quietly. Over twelve months, a $100 balance becomes anywhere from $76 to $88 before any transaction costs, depending on the platform's fee. On a balance near zero, some platforms continue charging, creating a negative balance that blocks future access.

This is not a scam. It is a fee buried in documentation that most users never read until they return to an account they thought was safely parked.

💡 The rule: Before leaving funds idle on any custodial platform, check three things: whether an inactivity fee exists, what the threshold period is, and what counts as activity sufficient to reset the clock. A single small transaction every five months is often enough to avoid the fee entirely.

Mistake 4: Withdrawing Small Amounts Frequently Instead of Batching

Every withdrawal carries a fixed fee component. When users withdraw small amounts often, that fixed fee becomes a disproportionate cost.

Consider a user who withdraws $50 ten times over a month versus once at $500. Assume a fee structure of $3 fixed plus 0.5%:

10 withdrawals × ($3.00 + $0.25) = $32.50 in fees

1 withdrawal × ($3.00 + $2.50) = $5.50 in fees

Same total amount moved, $27 difference — recovered by doing nothing except waiting.

For freelancers and remote workers receiving regular smaller payments, this matters. For businesses managing affiliate or contractor payouts, it matters more.

💡 The rule: If the fixed fee exceeds 1% of the withdrawal amount, wait and batch. In concrete terms: with a $3 fixed fee, do not withdraw less than $300 at a time — at that threshold the fixed fee is exactly 1%. Below $300, the fixed fee starts to dominate. For internal transfers between accounts on the same platform, the math often changes entirely — P2P transfers within Volet.com, for example, carry no fee at all.

Mistake 5: Swapping on a DEX Without Knowing Bots Are Watching

This mistake applies specifically to users who swap tokens on decentralized exchanges — Uniswap, Curve, PancakeSwap, and similar protocols. If you only use centralized exchanges or custodial platforms for conversions, it does not affect you directly. For traders and DeFi, it is one of the most consistent sources of silent loss in 2026.

MEV (stands for Maximal Extractable Value) refers to the profit that sophisticated bots extract from the blockchain by reordering, inserting, or front-running transactions before they are confirmed. The most common form affecting retail users is the sandwich attack.

Here is how it works in practice. You submit a transaction to swap $2,000 USDC for ETH on Uniswap. Before your transaction is confirmed, a bot detects it in the public mempool — the waiting area where unconfirmed transactions sit, visible to anyone. The bot immediately buys ETH ahead of you, pushing the price up slightly. Your transaction then executes at the higher price. The bot sells immediately after, pocketing the difference. Your trade went through. You received ETH. But you received less ETH than the quoted rate suggested, and the difference went to the bot.

The attack works because most users set a slippage tolerance to ensure their trade executes. A 1% slippage tolerance tells the protocol: execute this trade even if the price moves up to 1% against me before confirmation. That tolerance is the window the bot uses. The wider the tolerance, the larger the potential extraction.

Three things make a DEX trade more vulnerable: a wide slippage tolerance (above 0.5% on liquid pairs), a large trade relative to the pool's liquidity, and use of Ethereum mainnet where the mempool is fully public.

💡 The rule: Keep slippage tolerance as tight as the trade will allow — 0.3% to 0.5% on major pairs with deep liquidity. For larger trades, use MEV protection tools: Flashbots Protect, MEV Blocker, or CoW Protocol routes transactions through private channels that bypass the public mempool entirely, removing the bot's ability to front-run.

Splitting large trades into smaller amounts also reduces price impact per transaction. On Solana, MEV exists but sandwich attacks are structurally harder due to the network's architecture — this is one practical reason to prefer Solana for swaps when the asset is available on both networks.

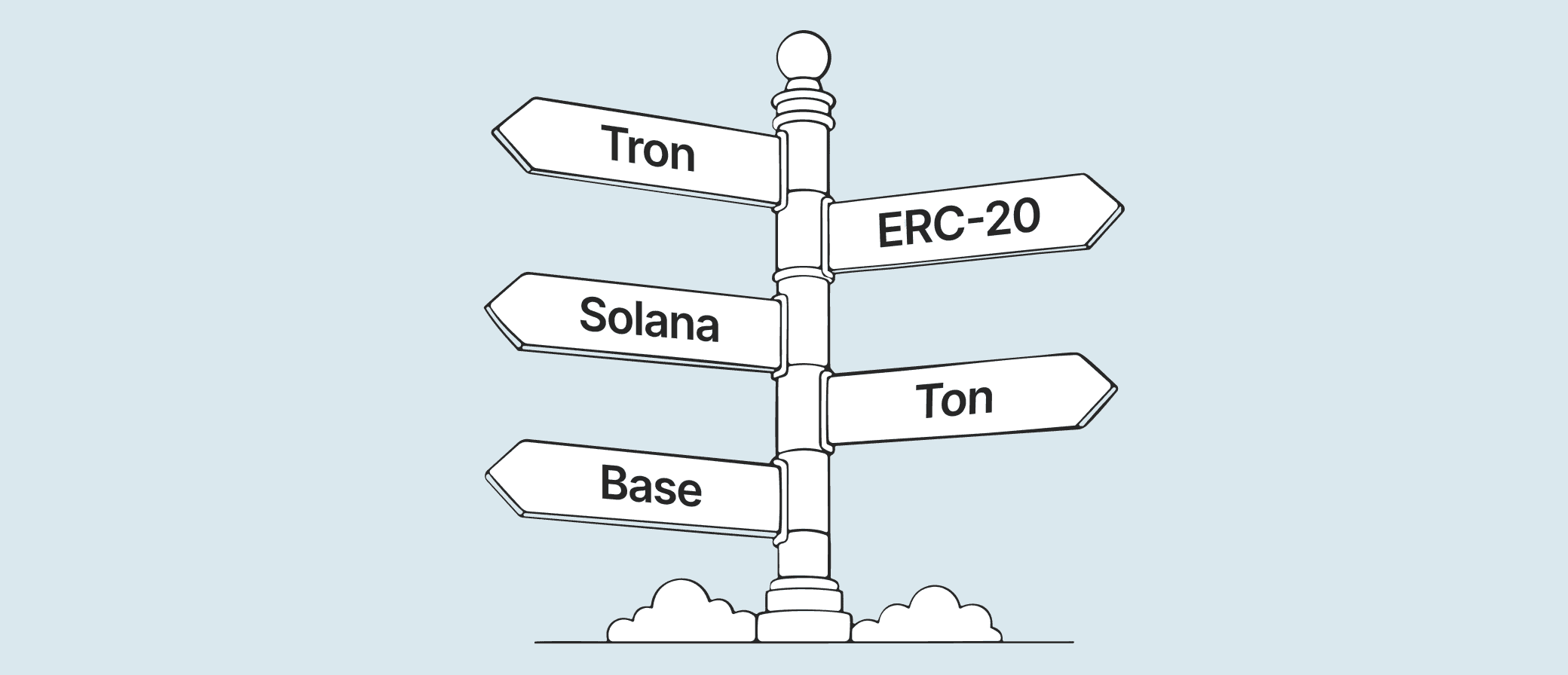

Mistake 6: Using an Expensive Network When a Cheap One Works

Most users pick a network once — usually Ethereum or Tron — and never reconsider it. That habit can cost more than the fees on the actual asset.

Network

Typical fee

When to use it

Ethereum L1

$0.10–$40+

Sending to a destination that only accepts ERC-20, no L2 support

Tron (TRC-20)

$2–$4

Sending to older exchanges that only list TRC-20 USDT — no better option available

Arbitrum / Base / Optimism

< $0.01

Sending to DeFi apps, exchanges that support L2, any ETH-ecosystem transfer

Solana

< $0.01

Sending SOL-native tokens, USDC on Solana, fast retail transfers

TON

< $0.01

Sending to Telegram wallets, TON-ecosystem apps

BNB Chain

$0.05–$0.20

Sending to exchanges that don't support L2 but accept BEP-20

A cheaper fee does not mean a less secure network. Arbitrum, Base, and Optimism are L2 networks built on top of Ethereum — transactions are ultimately settled and verified on Ethereum mainnet. The reduced fee reflects a more efficient approach to transaction batching, not a weaker security guarantee.

Solana processes over 300 million transactions per day and has a market capitalisation above $80 billion — figures that reflect years of real-world stress testing at scale. TON, the network behind Telegram's wallet infrastructure, handles hundreds of millions of users across the Telegram ecosystem. These are not experimental alternatives. They are mature networks that happen to cost a fraction of what Ethereum mainnet or Tron charge for the same transfer.

💡 The rule: For transfers under $500, use L2 networks, Solana, or TON. Reserve Ethereum mainnet for large amounts where the fixed fee is proportionally small.

Mistake 7: Granting Unlimited Token Approvals and Never Reviewing Them

Another mistake that applies to users who interact with DeFi protocols — lending platforms, DEXs, yield aggregators, and similar applications. If you only use centralized exchanges or custodial wallets, token approvals do not affect you.

When you use a DeFi protocol for the first time, it asks permission to access tokens in your wallet. Most interfaces default to unlimited approval — meaning the contract can move any amount of that token, at any time, for as long as the approval exists. You click confirm once, pay a small gas fee, and move on. The approval stays active indefinitely, even after you stop using the protocol.

Token approval is essentially a signed cheque with no expiry date. This creates silent, persistent risk. If a protocol is later exploited, hacked, or its smart contract is upgraded maliciously, an active unlimited approval gives the attacker direct access to your tokens — no further action required on your end. The approval you granted six months ago for a protocol you no longer use is still open.

💡 The rule: Pay particular attention to unlimited approvals on tokens you still hold. A reasonable habit: full approval audit every few months.After interacting with any new protocol, check what you approved. The standard tool for this is revoke.cash — an open-source project that has been a standard part of wallet hygiene in the crypto community for years. Connect your wallet, and the interface lists every active approval: the contract, the token it can access, and the spending limit.

Revoke.cash does not access your funds, does not store your seed phrase, and does not require any permissions beyond reading your approval history. Revoking an approval is a standard on-chain transaction — the same operation you can perform manually through a block explorer like Etherscan; revoke.cash simply makes it faster and readable. The transaction costs under $0.50 on most L2 networks.

Mistake 8: Chasing High Yields in DeFi Protocols

This mistake applies to users who deposit funds into yield-bearing DeFi protocols — staking pools, lending platforms, liquidity vaults, and similar instruments. If you hold funds only on centralized exchanges or custodial wallets, this does not affect you directly.

The logic is straightforward: a protocol offers 12–25% in average yield, the interface looks clean, and the token has a recognisable name. What the yield dashboard does not show is the smart contract risk underneath. Every deposit into a DeFi protocol is a bet not just on the yield, but on the security of the code that holds your funds.

The scale of the problem in 2026 is not theoretical. DeFi protocols lost $169 million across 34 hacks in Q1 2026, according to DefiLlama. April alone saw $606 million drained across 12 separate incidents in just 18 days. Recovery is rare: the recovery rate across March losses stood at 0.04% — $9 million of $137 million stolen.

The Resolv Labs incident triggered what analysts called a "shadow contagion" effect — losses spread to connected protocols that had nothing to do with the original breach. The USR stablecoin collapse created bad debt across Morpho Blue, Euler, and Fluid protocols — platforms that had nothing to do with the original breach but were downstream of it. This is how DeFi protocols are built: they depend on each other, and a failure in one propagates to others without warning.

The yield does not compensate for this risk at the retail level. A 15% yield on $5,000 generates $750 over a year. A single exploit that drains the protocol returns zero — and recovery, as the data shows, is almost never an option.

💡 The rule: Before depositing into any yield protocol, check three things:

Has the protocol been audited — and by whom? Audit reports are public; the absence of one is a signal.

How long has the protocol been live? Newer protocols carry higher undetected vulnerability risk.

Is your yield exposure concentrated in one protocol? Spreading across several reduces the impact of a single exploit.

For funds you cannot afford to lose, a custodial platform with lower yield and no smart contract exposure is the structurally safer choice.

Mistake 9: Keeping Long-Term Funds on a Trading Exchange Because It Feels Convenient

A trading exchange holds funds in a pooled structure optimised for high-frequency trading, margin positions, and liquidity. That structure creates a specific risk profile: exchange hacks historically target trading platforms because large pooled balances make them high-value targets. Exchanges also freeze withdrawals during periods of stress — sometimes without warning.

For funds you are not actively trading, use platforms designed for payment flows, not trading. The risk profile is different: the attack surface is smaller, there is no margin lending against user deposits, and there is no trading book that can go insolvent.

Neither model is risk-free — both require trusting the operator — but the type of risk and the scenarios under which you lose access to funds differ meaningfully.

💡 The rule: Keep on an exchange only what you need for active trading. Move the rest to a wallet designed for storage and payments, not for trading infrastructure.

One account, many exchanges

Buy and sell crypto and stablecoins at great prices quickly and seamlessly. Volet.com connects you to the best the crypto world has to offer.

If sending to an exchange or wallet platform, go to the deposit section, select USDT, and look at the network dropdown. The options listed there are the networks the platform actually monitors — any network not listed will result in funds that never appear.

If sending to a person or business, ask them to check their deposit page and share the exact network name alongside the address.

Never infer the network from the address format: Ethereum, Arbitrum, BNB Chain, Polygon, Optimism, and Base all use the same 0x address format but are separate networks. The address alone tells you nothing about which one applies.

Yes. L2 networks — Arbitrum, Optimism, Base, and similar — inherit Ethereum's security model. Transactions are ultimately settled and verified on Ethereum mainnet; the L2 layer handles execution more efficiently.

The reduced fee does not reflect reduced security — it reflects a different approach to transaction batching, not a weaker underlying guarantee.

The practical consideration is the same as with any network: confirm the recipient supports that specific L2, then send a test amount first.

The logic makes sense in theory: if crypto-to-stablecoin conversion is cheaper than crypto-to-fiat, and stablecoin-to-fiat withdrawal is cheaper than crypto-to-fiat withdrawal, then the two-step path saves money.

In practice this varies. Some platforms charge a conversion fee at each step, meaning two conversions cost more than one direct path. Others offer free or near-free stablecoin-to-USD conversion, making the intermediate step genuinely cheaper.

The way to check: calculate the total cost of both paths before initiating either. Step one: find the crypto-to-stablecoin conversion fee. Step two: find the stablecoin withdrawal fee. Add them and compare to the direct crypto-to-fiat withdrawal cost. Whichever total is lower is the right path for that platform and that amount.

No. MEV and sandwich attacks apply to DEX trades — swaps executed directly against liquidity pools on decentralized exchanges.

When you accept crypto payments through a payment gateway or custodial platform, your customers send funds to an address you control (or that the platform controls on your behalf), and that transaction is a simple transfer, not a DEX swap. There is no liquidity pool involved, no slippage tolerance to exploit, and no public mempool exposure in the same sense. MEV bots have no mechanism to extract value from a payment transfer.

The only scenario where MEV becomes relevant for a merchant is if you actively swap received crypto into a different asset using a DEX — for example, converting received ETH to USDC yourself through Uniswap. In that case, the swap itself is subject to the same MEV risks as any other DEX trade. If you use a platform that handles conversion automatically on your behalf through a centralized mechanism, you are not exposed.

First, find the current mid-market rate for the pair you want to convert — go to CoinGecko or CoinMarketCap and look up the asset price in your target currency. This is the real rate, without any platform markup.

Second, go to your platform and initiate a conversion — but do not confirm it yet. Look at the rate the platform is offering.

Third, divide the platform rate by the mid-market rate and subtract one. If the mid-market rate for USDT/USD is 1.000 and your platform offers 0.988, the spread is 1.2%.

Fourth, multiply that percentage by the amount you are converting to get the spread cost in dollars. On $5,000 at 1.2% spread, that is $60 that does not appear anywhere as a line item.

If the platform does not show you a conversion rate before confirmation — only a final amount — work backwards from the amount to calculate the implied rate and compare it to mid-market.