The right way to adopt crypto payouts at scale isn't a complete overhaul — it's a test. Run it next to what you already have, measure the gap, and let the numbers speak for themselves.

If you are reading this, you probably already have a payout system — Payoneer, SWIFT, card payouts, or some combination. The question isn't whether to add crypto to your mass payout solutions. It's how to do it without creating new operational problems, and without forcing thousands of partners to change how they receive money all at once. This guide covers how to audit what you have, identify where crypto adds the most value, and run a migration that doesn't break what already works.

1️⃣ Audit What You Have

Before choosing a platform or writing a line of API code, map where your current system is actually breaking down. The corridors that are most painful today are the right places to start with crypto — not the entire payout program at once. Start with answering these questions.

Where are you losing money on fees? International wire transfers to Southeast Asia or Africa, card payouts at 4.5%+, or Payoneer transfers to markets where their margins are highest — these are the corridors where crypto delivers the fastest ROI. Calculate your actual cost-per-transaction by corridor, not just overall.

Where are you failing to deliver at all? Some markets have no reliable fiat path. If you have partners in Nigeria, Bangladesh, or certain parts of Latin America who consistently have problems receiving payments, crypto is often the only infrastructure that works.

Which partners have already asked for USDT? In many networks handling crypto affiliate payouts across global coverage, a significant share of affiliates and contractors — often between 20–40% — are already comfortable with crypto. These are your pilot group — they'll switch without friction and give you operational data before you touch the rest of the base.

What does your current reconciliation cost in time? If your finance team typically spends 15+ hours per payout cycle on manual verification and reporting — especially for international contractor payouts across multiple geographies — that's a fixed cost that automation via API eliminates regardless of which payment method you use.

Common mistake: making the decision in the abstract — "should we do crypto?"

Smart way: running an hour-long audit that tells you which corridors to migrate first, which partners to onboard in the pilot, and how to frame the business case internally.

2️⃣ Choose the Right Payout Model

There are three commonly used architectures for mass payouts. Each suits a different operational profile.

Platform-initiated payouts via API

It’s the right model for CPA networks, affiliate programs, and any platform where the business controls the timing and calculates the amount. Your system detects a qualifying event — a confirmed deposit, a completed lead, a revenue threshold crossed — and fires a payout request directly through the API. No manual steps, no spreadsheet uploads, no finance team involvement per transaction.

Payouts go out the moment the condition is met; no one needs to remember to run a batch. This model scales to thousands of payouts per minute, giving you complete control: receive real-time webhooks on transaction status, query balances, and embed payout logic directly into your platform's event flow.

At its core, this is what a proper automated payout system looks like: event-driven, zero manual intervention, and auditable at every step.

Volet.com's bulk crypto payments API is free to connect, has no monthly subscription, and charges only on processed transactions. The scope of integration depends on what you're building — a simple batch trigger is a day's work; a fully embedded payout engine with retry logic and status monitoring is a week or two.

This one works best for iGaming platforms, creator economies, exchanges, and marketplaces where recipients request their earnings on demand. The platform doesn't push money — it responds to withdrawal requests.

Recipients control timing, which measurably improves their retention and satisfaction. And Volet.com's infrastructure handles the execution.

Manual payouts via dashboard or CSV upload

This approach suits agencies, startups in early stages, and any business running fewer than a few hundred global mass payouts per month. Upload a file with wallet addresses and amounts, review the batch, confirm. It is the practical starting point for operations teams without immediate development resources.

Volet.com supports this workflow alongside API access, so teams can validate the process manually before committing to full automation.

With 200 payouts a month, a spreadsheet is enough — each new partner adds roughly the same amount of work. Past that point, exceptions multiply faster than volume: failed transactions, wrong addresses, missed payments, partner follow-ups.

That's exactly when API automation helps by detecting errors instantly, knowing exactly which transaction failed, and retrying it automatically instead of hunting through a spreadsheet

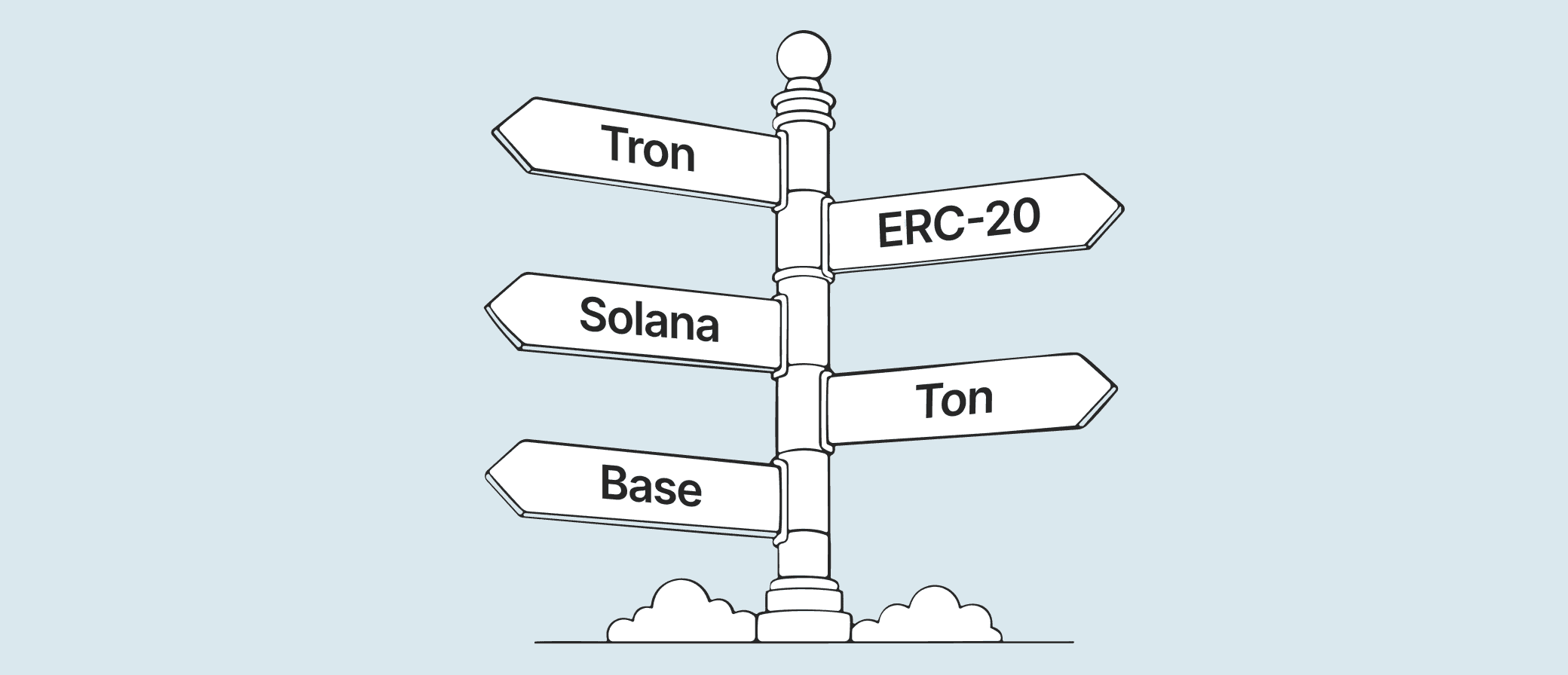

3️⃣ Pick the Right Blockchain

Network selection is the most consequential technical decision in building a crypto payout system, and most teams make it by inertia rather than analysis.

Here is the actual cost structure across major networks:

Network

Fee per transaction

L2 Ethereum (Arbitrum, Base, Optimism)

< $0.01

Solana

< $0.01

TON

< $0.01

Ethereum (L1)

$0.05–$0.40

Tron (TRC-20)

$1–$2.50

The main trick here is with Tron. It became the default network for USDT transfers because it was fast and cheap — in 2019. Today it is consistently the most expensive option for mass payouts. A business sending 1,000 payouts per month in USDT on Tron spends $1,000–$2,500 in network fees alone per batch. The same batch on Arbitrum or Base costs under $10.

Practical routing logic

▪️ Average payout over $50: any low-cost network works; optimize for recipient's existing address format.

▪️ Micro-payouts under $10: use L2 networks (Arbitrum, Base) or internal platform wallet transfers where the fee is percentage-based rather than fixed.

▪️ Mixed recipient pool: run two networks in parallel, route by recipient's registered address format.

Despite this, many platforms still default to Tron because recipients are used to it, especially in emerging markets. The solution is routing to a managed platform wallet — such as Volet.com — where the recipient receives in a stable dollar balance and withdraws in their preferred method.

4️⃣ Solve the Last-Mile Problem

This is the part most platforms miss, and where payout systems fail in production.

A partner in Nigeria receives USDT on their wallet. What happens next? If your platform selected a payment infrastructure with no off-ramp for their local currency, the partner holds digital dollars they cannot convert to real money without going through a third-party exchange, paying additional fees, and completing a process your platform has no visibility into.

This is the last-mile problem, and it is the difference between "we support payouts to Nigeria" and "our partners in Nigeria actually get paid." Solving it is what separates a functional global payout platform from one that works only in theory.

There are three structural approaches:

Custodial wallet with built-in off-ramp: The recipient receives funds on a platform wallet — such as Volet.com — and can withdraw in their local currency via local bank transfer or card. The platform never touches the conversion; the recipient handles it at their discretion, using a system designed for their market. This is the cleanest architecture for global programs.

Direct on-chain to external wallet: Works well when recipients are crypto-native and prefer to manage their own funds. Requires no off-ramp infrastructure from your side — but also offers no help if a recipient gets stuck converting to local currency.

What if your partners don't want to deal with crypto at all

This is more common than most platforms expect — particularly among freelancers and affiliates in traditional markets who are comfortable receiving bank transfers but have never held a stablecoin.

The practical solution is a managed wallet approach: your platform pays out to a Volet.com wallet, and the recipient then withdraws in their local currency via bank transfer or card, without ever needing to understand the crypto layer underneath. They see a balance in dollars; the crypto is invisible to them.

The Cost Math for 1,000 payouts per month, average amount $200

Method

Fee per transaction

Monthly fee total

International wire transfer

$30–50 (sending fee only)

$30,000–$50,000+

Card payout (business mass payouts)

from 2.5%

~$5,000+

Automated stablecoin payout via L2

< $0.01 network + from 0.25%

~$500–$600

Internal wallet payout (Volet.com)

from 0.5%

~$1,000

Two things this table doesn't show: first, the L2 network fee is fixed regardless of amount — so at $200 per payout, 0.25% + $0.01 is clearly cheaper than 0.5%. But at $2 per payout, a fixed $0.50 network fee becomes 25% of the transaction, while 0.5% of $2 is $0.01. Key takeaway: Internal wallet transfers win decisively for small amounts.

Second, L2 payouts require the recipient to have an L2-compatible wallet address — which many affiliates in emerging markets don't have. Internal wallet payouts work for any recipient regardless of crypto experience.

5️⃣ Avoid Most Common Pitfalls

Transaction failures: Blockchain transactions can be rejected during network validation. In a batch of 5,000 payouts, even a 0.5% failure rate means 25 transactions that didn't land, and those failed transactions still consume the network fee. Your payout infrastructure must track each transaction's status, flag failures immediately, and support retry logic.

And that’s where full API integration gives you complete control: trigger payouts programmatically, receive real-time webhooks on transaction status, query balances, handle exceptions automatically, and embed payout logic directly into your platform's event flow.

Sequential vs. parallel execution: If your system sends transactions one after another, 5,000 payouts even on a network with only 2-second confirmation time takes nearly three hours. Mass payout automation — executing batches in parallel streams — is what compresses the same volume to minutes.

Volet.com's infrastructure executes batches in parallel streams, compressing the same volume to minutes. This matters for time-sensitive payouts — real-time affiliate settlements.

Balance management: Unlike credit-backed payout systems, crypto payouts require pre-funded balances, so your liquidity must cover the next payout cycle at all times. To handle this Volet.com supports multiple funding methods via SWIFT, SEPA, FPS, CIPS, local bank transfers, or crypto (7 currencies across major networks).

You can hold your operating balance in USD or EUR — and pay out in crypto or stablecoins with automatic conversion at the moment of each transaction. This means your treasury stays in fiat while your partners receive USDT, USDC, or other crypto, with no volatile assets on your books and no daily revaluation overhead.

Compliance and recipient data: Paying thousands of affiliates via crypto doesn't eliminate the need to know who you're paying. Global anti-money laundering frameworks require that payout platforms screen transactions against sanctions lists and maintain records of recipients. The good news: a reputable payout platform handles the AML screening infrastructure; your job is to collect and pass clean data at onboarding, not to run compliance checks yourself.

6️⃣ Migrate Without Breaking What Works

The goal isn't to replace your existing payout system on day one. It's to run crypto in parallel until the new infrastructure earns the right to take on more volume.

Step 1: Pick your pilot corridor. Start with the segment where your current system hurts most — the highest-fee corridor, the geography with the most failed payments, or the partners who've already asked for USDT. A good pilot group is 30–100 affiliates or contractors: large enough to generate meaningful operational data, small enough that problems are manageable. If your payout cycle is monthly, one cycle is enough to validate the basics.

Step 2: Onboard them before the payout, not during. The biggest migration mistake is announcing crypto payouts and then scrambling to collect wallet addresses at settlement time. Send a dedicated communication two weeks before the first crypto cycle explaining what's changing, why, and what each partner needs to do — typically, registering on the platform and verifying their withdrawal method. Make it optional for now; you're not mandating a change, you're offering an option.

Step 3: Run parallel, not replacement. For the first cycle, keep your existing payment method active for everyone who doesn't opt in. This removes the deadline pressure that causes address errors and rushed onboarding. Measure cost, speed, exception rate, and how much time your finance team spent — against your current baseline for the same corridor.

Step 4: Audit your existing address base. If you have a database of partner payout details, treat it as suspect until verified. Exchange addresses rotate, network preferences change, people switch platforms. Before migrating any partner, require a fresh address confirmation — ideally validated with a small test transaction. This one step prevents the majority of misdirected payments.

Step 5: Scale to the next corridor. Once the pilot is clean, repeat for the next-highest-friction corridor. Don't try to migrate everything at once. The networks, the platforms, and your own operations team all need time to stabilize before adding volume.

Start global payouts today — in crypto and fiat

Reach creators, partners and teams in any country with payouts in USDT, USDC or to Volet.com wallets.

It depends on the payout destination and the platform you use. For crypto affiliate payouts sent directly on-chain transfers to an external wallet, many platforms require only a wallet address — no identity verification on the recipient's side. For international contractors payouts routed to a managed platform wallet (like Volet.com), the recipient typically completes a lightweight verification to unlock withdrawals to bank accounts or cards.

The business sending the payouts completes KYB (Know Your Business) verification — which is a one-time process, usually taking less than a day. Beyond that, a reputable global payout platform handles AML screening and sanctions checks in the background; you don't manage that process directly.

Yes — and for most finance teams, this is the right architecture for automated stablecoin payouts, because holding crypto on a company's balance sheet creates accounting overhead.

The practical solution is to fund your payout account in USD or EUR via bank transfer, hold the operating balance in fiat, and let the platform handle automatic conversion to crypto at the moment of each payout. This is exactly what mass payout solutions built for scale are designed to support — your treasury stays in stable, auditable fiat. Your partners receive USDT or USDC.

Volet.com supports this flow natively — you can fund via SWIFT, SEPA, or local bank transfer, hold in USD or EUR, and pay out in stablecoins or crypto across 9 and 7 networks respectively, with conversion handled automatically at settlement.

The short answer: yes, in most markets — but the rules vary significantly by country and are evolving quickly. Crypto payouts to contractors and affiliates are legal in the vast majority of jurisdictions where Volet.com operates. The critical requirement is using a regulated, AML-compliant platform rather than sending directly from a company wallet with no compliance layer.

Any automated payout system worth deploying at scale must be built on regulated, compliant infrastructure — not just technically sound, but legally defensible. Whether you rely on a bulk crypto payments API or a dashboard-based workflow, the platform's compliance layer is what makes global operations sustainable.

The practical question for your finance and legal team is not "is crypto legal here?" but "what documentation do we need for this payout to be auditable?" That means maintaining clear records of who received what and when, which a proper payout platform provides as a standard export.

It's a real operational risk — especially when global mass payouts are time-sensitive and your partners are spread across multiple time zones. Any single provider can experience downtime, banking partner disruptions, or network congestion at the wrong moment.

Mass payout automation helps here: when your system runs programmatically with retry logic and real-time status monitoring, a transient failure doesn't mean a missed payment cycle — it means an automatic retry. But infrastructure-level downtime is a different problem.

The practical approach: maintain a secondary payout method — either a second provider integrated via API, or a manual fallback for emergency batches — so that a platform issue doesn't become a partner crisis.

This doesn't mean splitting your entire volume across multiple providers from day one. Start with one platform, validate the process, then add a backup for your most critical corridors. The integration cost is low relative to the operational insurance it provides.

This varies by country, but the most common path is through local P2P exchanges, crypto OTC desks, or regional exchange platforms that support local bank deposits.

Where you can help is by choosing a payout infrastructure that gives the partner an on-ramp to local currency if they need it.

Volet.com wallets cover local bank transfer withdrawals in 20+ currencies, including currencies across Southeast Asia, Africa, and Latin America — so partners who prefer not to use P2P platforms have a built-in conversion path.